Anti-Money Laundering (AML) regulations play a crucial role in maintaining the integrity of financial systems worldwide.

While Anti-Money Laundering (AML) regulations are primarily associated with financial systems, their relevance extends beyond the financial sector. AML measures are designed to combat the illicit flow of funds and prevent the integration of illegally obtained money into the legitimate economy. As a result, various industries and sectors are subject to AML regulations to varying degrees.

In the United States, AML efforts are multifaceted and comprehensive, they involve a combination of legislative frameworks, regulatory agencies, and legal enforcement mechanisms.

The primary legislation addressing these issues is the Bank Secrecy Act (BSA), enacted in 1970. The BSA aims to prevent money laundering by requiring financial institutions to maintain certain records and file specific reports that could help identify and prevent illicit financial activities.

The US Bank Secrecy Act (BSA) and its Key Components:

The Bank Secrecy Act (BSA) is officially known as the Currency and Foreign Transactions Reporting Act, it was enacted in 1970 in response to concerns about money laundering and other financial crimes.

Post WW II, there was growing concern about the influence of organized crime in the United States in particular. The war had had profound effects on global geopolitics, economics, and the emergence of organized crime, thus setting the stage for the subsequent concerns addressed by the BSA. Criminal organizations were involved in a range of illegal activities, including racketeering, drug trafficking, and money laundering.

The Cold War era that would follow also brought about heightened national security concerns. Governments, including those of the United States, became increasingly focused on tracking and countering activities that posed a threat to national security. Illicit financial activities, including money laundering, were recognized as potential tools for supporting espionage, subversion, and other security risks.

The post-war period also marked the beginning of the modern era of international finance and international finance systems. The Bretton Woods Agreement in 1944 established a new international monetary system, and the subsequent decades saw the growth of what we now consider “global financial institutions”.

As financial systems became more interconnected, policymakers recognized the need for mechanisms to track and combat illicit financial activities across borders. This recognition was focused in part, on the need for legislation to address many related issues and generally disrupt the financial networks supporting organized crime.

Legislation is often enacted as a tool to address Tax Evasion and reign in Underground Economic Activity

Throughout history, governments have implemented laws to combat tax evasion and regulate economic activities conducted outside the formal sector. During the prohibition era of the 1920s through the early 1930s, the US government enacted legislation to regulate and tax the production and sale of alcoholic beverages, aiming to curb underground economic activities associated with illegal alcohol production. This spawned iconic drama in the form of television programs, cinema, and stage. Such legislation was successfully used to capture and imprison famous criminals like Al Capone.

In recent years, there have also been initiatives of a more global nature, that have pushed to address tax evasion and promote financial transparency. Initiatives such as the Common Reporting Standard (CRS) and the Automatic Exchange of Information (AEOI) were introduced to facilitate the exchange of financial information between countries, making it more challenging for individuals and entities to hide income and assets in offshore accounts.

As the U.S. government was grappling with challenges related to tax evasion and the existence of a sizable underground economy the authorities observed that large cash transactions and the movement of funds evaded taxation and were contributing to government revenue losses. The government sought tools to track and monitor financial transactions more effectively with legislation like the BSA.

The Organized Crime Control Act was signed into law by President Richard Nixon on October 15, 1970. This included Title II, which is known as the Bank Secrecy Act. This legislation marked a significant step in addressing various concerns. It required financial institutions to keep records and file reports that could assist law enforcement in uncovering and preventing financial crimes.

The BSA is the cornerstone of the U.S. AML regulatory framework. Financial institutions, including banks, credit unions, and money service businesses, are mandated to establish AML programs. These programs must include policies and procedures to detect and report suspicious transactions to FinCEN.

Several regulatory agencies oversee AML compliance in the U.S., including the Office of the Comptroller of the Currency (OCC), the Federal Reserve, and FinCEN.

The BSA also led to the establishment of the Financial Crimes Enforcement Network (FinCEN) in 1990. FinCEN is a bureau of the U.S. Department of the Treasury that administers and enforces the BSA. FinCEN also serves as a hub for collecting, analyzing, and disseminating financial intelligence to combat money laundering and other financial crimes.

FinCEN is the main regulatory authority responsible for collecting and analyzing financial transaction data to combat money laundering and other financial crimes.

Given the global nature of financial transactions, international cooperation is vital in the fight against money laundering and terrorism financing. The US actively collaborates with other countries and participates in global initiatives to strengthen AML measures. Organizations such as the Financial Action Task Force (FATF) set international standards, and countries, including the U.S., align their AML frameworks with these standards.

Counter Terrorism Concerns

While the initial focus was on organized crime and tax evasion, later amendments to the BSA incorporated provisions related specifically to trying to deal with the financing of terrorism. Global awareness of the link between financial systems and terrorist activities grew, particularly post 9/11, and regulatory frameworks were adapted to address these concerns.

The focus on counter-terrorism within the U.S. Bank Secrecy Act (BSA) intensified notably with the passage of the USA PATRIOT Act in 2001. The BSA was now to become a critical component of the U.S. government’s efforts to combat terrorism financing.

The Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act (USA PATRIOT Act) was enacted in response to the terrorist attacks on September 11, 2001 (9/11). This legislation introduced significant amendments to various existing laws, including the BSA, to enhance the government’s ability to combat terrorism and protect national security..

Section 311 of the USA PATRIOT Act specifically grants the Secretary of the Treasury the authority to take special measures to address money laundering or other financial crimes that pose a significant threat to the U.S. financial system. This authority allows the Secretary to impose specific regulatory measures on financial institutions and transactions involving jurisdictions, financial institutions, or classes of transactions identified as primary money laundering concerns.

Expanded Reporting Requirements

The USA PATRIOT Act broadened the scope of the BSA’s reporting requirements to cover not only traditional money laundering but also activities related to terrorist financing. Now, financial institutions were mandated to report suspicious transactions that could be linked to potential terrorist activities.

The Act required financial institutions to establish and maintain robust Customer Identification Programs (CIPs) to verify the identities of their customers. This measure was aimed at preventing terrorists from using the financial system to move funds anonymously.

The USA PATRIOT Act also encouraged and in some cases mandated greater information sharing and coordination between financial institutions and government agencies. This facilitated a more collaborative approach to identifying and disrupting potential terrorist financing activities.

The Act included provisions addressing “foreign correspondent accounts”, and imposing additional due diligence requirements on financial institutions dealing with foreign banks.

“Foreign correspondent accounts” are financial accounts held on behalf of another financial institution, typically from foreign countries. Such accounts facilitate the cross-border movement of funds and the provision of banking services between institutions in different jurisdictions. Foreign correspondent accounts play a crucial role in international finance, allowing banks to engage in transactions, settle payments, and conduct other financial activities on behalf of their foreign counterparts.

Policymakers recognized the importance of gathering financial intelligence to identify and disrupt criminal and illicit activities. The BSA was now enhanced to provide the authorities with the necessary tools to collect information on large cash transactions, suspicious activities, and potential money laundering schemes.

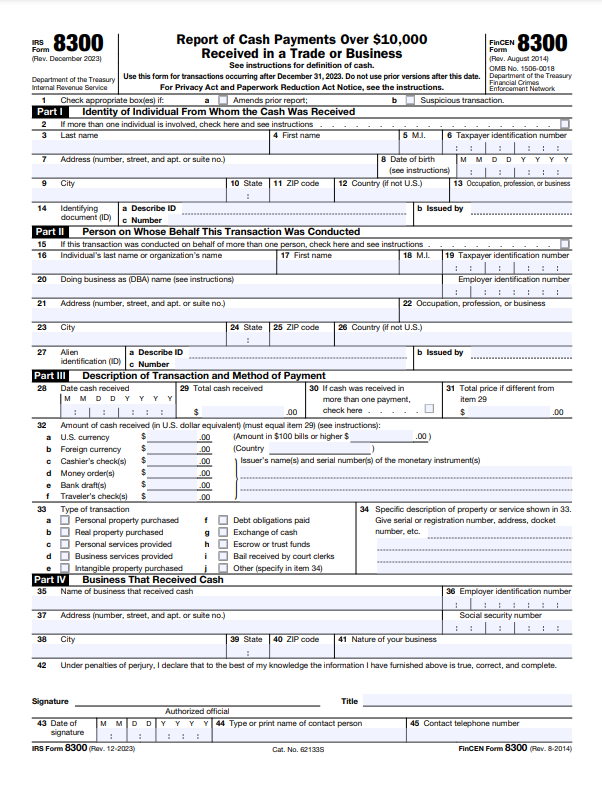

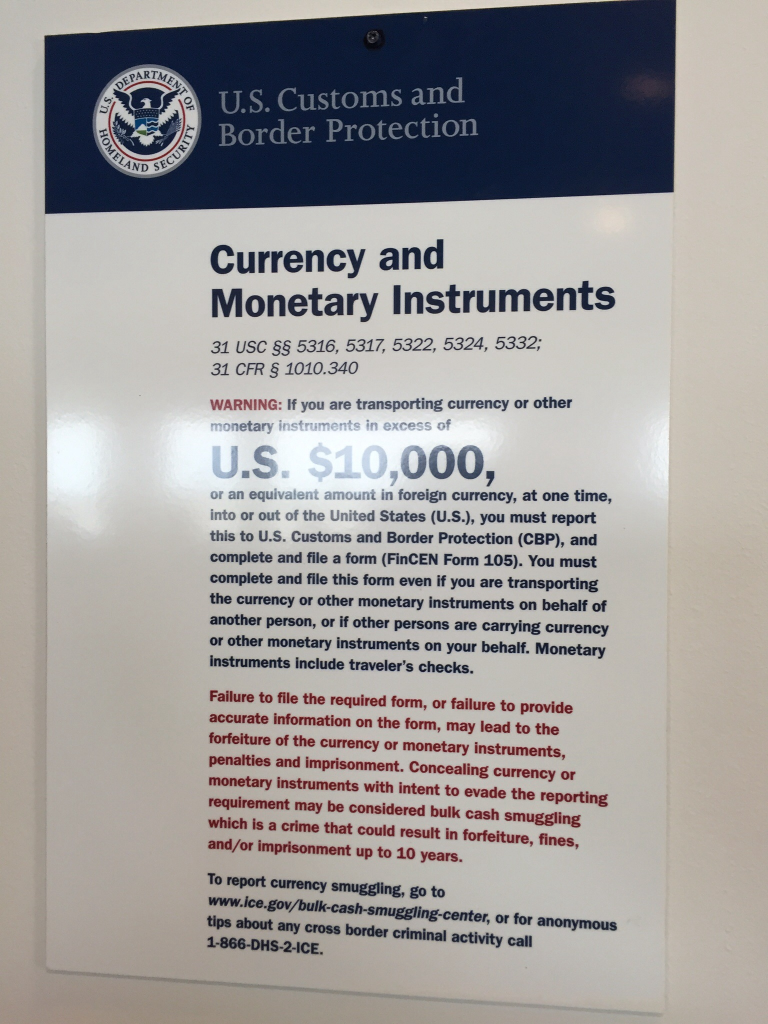

One of the aspects that the general public will more visibly recognize as a direct result of the BSA is the filing of Currency Transaction Reports (CTRs) for transactions exceeding $10,000 in cash. Additionally, Suspicious Activity Reports (SARs) are crucial for reporting transactions that may indicate potential money laundering or other illicit activities. Warnings about carrying large amounts of cash across international borders are visible at airports in all corners of the globe

|  |

AML Compliance for Different Sectors

AML obligations exist for various sectors. Financial institutions, such as banks and credit unions, bear a significant burden due to their central role in the financial system. However, other industries, include casinos, money services businesses, and even certain non-financial businesses and professions.

Financial Institutions are required to establish and maintain robust AML programs, conduct customer due diligence, and report suspicious transactions.

Certain non-financial businesses, such as casinos, real estate agents, and dealers of high-value goods are also often subject to AML regulations. This is because such businesses can be conduits for money laundering, and the regulations aim to mitigate this risk.

Lawyers, accountants, realtors, and other professionals who handle financial transactions or provide services are increasingly subject to AML regulations. This helps prevent the misuse of professional services for illicit financial activities.

CMDM’s role in a CIP

A Customer Master Data Management like the Pretectum CMDM system can play a valuable role in supporting a Customer Identification Program (CIP) within the financial industry.

A CIP as mentioned, is a regulatory requirement under anti-money laundering (AML) and Know Your Customer (KYC) regulations. It mandates that organizations implement procedures to verify and document the identity of customers.

The CMDM system acts as a centralized repository for customer data. It consolidates and manages customer information from various sources and business units within the organization. This centralized approach ensures that accurate and up-to-date customer data is readily available for the CIP process.

CMDM systems help maintain data quality and accuracy by enforcing data governance policies. They facilitate the standardization of customer data, ensuring consistency across the organization. Reliable and accurate data is essential for effective customer identification and verification during the CIP process.

The CMDM system provides a single, comprehensive view of each customer by integrating data from different channels and business units. This holistic view aids in understanding the customer’s relationship with the institution, supporting a more thorough CIP. It helps prevent identity-related fraud by ensuring that all relevant information is considered during customer identification.

In terms of identity verification, the CMDM can consolidate various forms of identification data, such as government-issued IDs and other supporting documents as details supporting KYC. This centralized data repository simplifies the process of cross-referencing and validating customer information against authoritative sources, contributing to a robust CIP.

Importantly, CMDM systems support the entire customer data lifecycle, from onboarding to ongoing monitoring. This is critical for CIP compliance, as customer information needs to be regularly reviewed and updated. The CMDM system ensures that any changes in customer data are captured, validated, and reflected in the customer’s profile.

CMDM systems allow for the integration of risk assessment modeling based on customer attributes. By categorizing customers into different risk segments, financial institutions can tailor their CIP procedures accordingly. This ensures that higher-risk customers undergo more rigorous identity verification processes as required by regulatory guidelines.

A well-integrated CMDM system seamlessly interfaces with CIP processes, providing a standardized approach to capturing and verifying customer information, reducing redundancy, and improving operational efficiency. The integration ensures that CIP processes leverage the most recent and accurate customer data.

Finally, CMDM systems like the Pretectum CMDM maintain a comprehensive audit trail of changes to customer data, supporting regulatory compliance and reporting requirements. This feature is crucial for demonstrating adherence to CIP procedures and responding to regulatory inquiries.

Anti-Money Laundering (AML) regulations are enforced around the globe through regulations like U.S. Bank Secrecy and PATRIOT Acts. AML compliance extends globally, necessitating collaboration exemplified by initiatives like the Common Reporting Standard. The Customer Master Data Management (CMDM) system, presented by solutions like the Pretectum CMDM, are an essential tool supporting Customer Identification Programs, centralizing and enhancing customer data for robust identity verification. The synergy of evolving AML regulations and technological solutions reflects a concerted global effort to fortify financial systems against diverse and evolving threats; CMDM can help in support organizations in having a more robust Customer Identification Program and help them to stay compliant.

Additional Reading: